You are not logged in.

Champagne: The Prestige

For a while it looked like Champagne was losing its lustre, but Lucy Britner finds more consumers being attracted to quality

In magic, there is a term called The Prestige. It refers to the third and most difficult part of a trick. It’s the most captivating, awe-inspiring and, well, magical part. For a while, it felt like Champagne wasn’t reaching The Prestige. It felt like it was just another sparkling wine.

But it’s not – and it never will be. In one sentence, Comité Champagne director of communications Thibaut le Mailloux tells us why there’s plenty of magic: “Champagne does not aim to quench the thirst of the global market for sparkling wines.”

Champagne has never been just another sparkling wine and, for many reasons, it has never really been a wine in the marketing world. It is more akin to a spirit in the way it plays the brand card. Indeed, 90% of Champagne’s global exports are from houses, rather than growers, according to the Comité Champagne. This could explain why, in some parts of the world, it is not the non-vintages that are gaining momentum, it’s Champagne’s own va va voom – vintages and prestige cuveés. Like limited-edition whiskies, vintages and prestige cuveés are unique, finite, exclusive and, above all, desirable.

Mailloux says: “Some countries, such as Japan, are particularly keen on enjoying special cuvées and vintage Champagne. Prestige cuvées, with almost 1 million bottles sold in Japan last year (2012), represent around 11% of the Champagne shipments to Japan and account for 29% of the value. Among Champagne’s 10 largest markets, Hong Kong, the US and Italy all import a considerable proportion of prestige cuvées within their Champagne repertoire.”

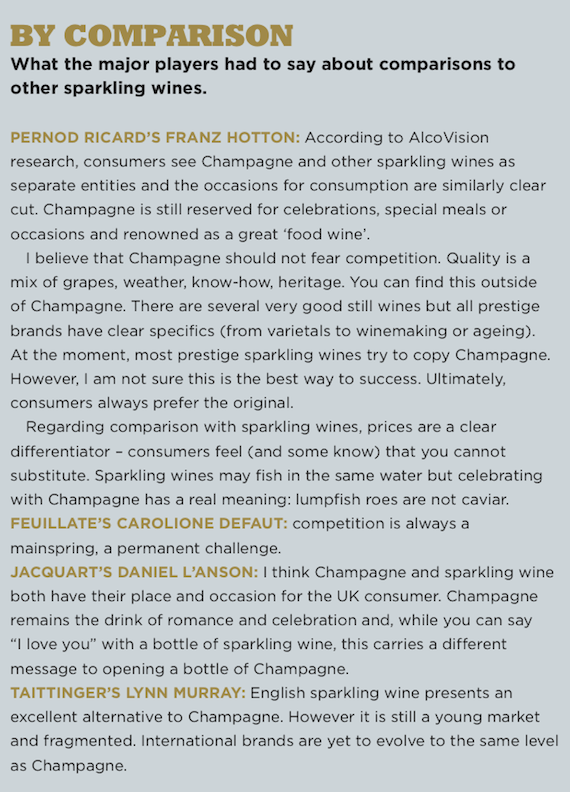

In the Pernod Ricard Champagne camp, prestige and vintage have long been important. Franz Hotton, international commercial director for Martell, Mumm and Perrier-Jouët says: “We have been witnessing a prestige upward trend for some while now.

In fact, the 2012 IWSR Report indicates a 3% increase in volume sales of super-premium Champagnes – so it seems that, despite the recession, consumers are increasing their consumption of luxury products. There are undoubtedly signs of a healthy prestige drinks market development.”

For a business that boasts both Asian and South American success for its two blended whisky brands – Chivas Regal and Ballantine’s – it’s no surprise that Pernod Ricard knows what it’s doing when it comes to launching limited-edition Champagnes in up-and-coming markets. The company launched Belle Epoque Florale Edition in markets including Japan and Brazil in 2012. Japanese artist Makoto Azuma created a floral artwork which was incorporated into the bottle design and this is the first limited edition of the cuveé Belle Epoque.

But for brands that don’t have the distribution power of Pernod Ricard, caution is key to succeeding in new markets. Centre Vinicole Champagne’s Nicolas Feuillatte brand sold 9.1 million bottles in 2012 – its second most successful performance ever. Despite a 6% fall in volume, the brand has retained its value, according to the company.

Nicolas Feuillatte marketing & communications manager Caroline Defaut says the company is “very careful with breaking into new markets”. She adds: “Opening in new markets is important but building a strong brand is even more important to us. Emerging countries are crucial but their Champagne culture still needs to be developed,” she says.

“Some of these emerging countries are just inaccessible because of the customs charge to pay. We recently entered China, Brazil and Thailand. We are also currently working on India. We are aware these developments will take time and we really want to develop a long-term relationship with our partners.”

Among Feuillatte’s releases for 2013 are: Grand Cru Chardonnay 2005, Cuvée 225 Brut 2005 and Palmes d’Or Brut 2002. Even in mature markets such as the UK – which, despite a loss of 6%, is still Champagne’s largest export market and almost twice the size of number two, the US – brands are finding favour with prestige, though vintage is not so hot.

Daniel I’Anson, Champagne Jacquart business development manager, UK, says: “We have seen that vintage is shrinking as a category in the UK, now representing around one eighth of the volume of rosé. Prestige Champagne sales are increasing in volume and value as consumers see a tangible reason to trade up. “In the UK, we have a short range of just five styles – Brut Mosaïque, Rosé, Blanc de Blanc Vintage, Extra Brut, and (to be launched soon) a new vintage Prestige Cuvée.”

Lynn Murray from Taittinger distributor Hatch Mansfield says interest in prestige cuveés “rings true but varies from market to market”. She says: “In the UK our business is stable but we have seen serious interest in our prestige cuvée Comtes de Champagne and there has been a great deal of interest in and demand for this wine and, in particular, big formats,” she says.

Paul Beavis, MD of Lanson International UK & general manager North America says Champagne is flying in the UK on-trade. “Here, champagne is growing at 7.2% versus sparkling at 5.5% in value”, he says. Beavis adds: “The top two Grandes Marques brands are driving value back into the market.” He claims growth is being led by his own brand with a 13.2% value boost.

The Champagne ceiling

There is another reason value is a much more attractive proposition than volume for Champagne – planting is at its limit and it will be years before any decision is made about extending the boundaries, then several more years on top of that before any grapes can be used to make Champagne. Therefore, value growth is not just a desire, for many it’s a necessity.

L’Anson says: “Champagne is now focusing more on maximising value as production is close to the ceiling of what can be produced in the region. Grape costs are becoming a more significant proportion of the cost of a bottle and this is pushing houses towards a more value-based strategy. The days of the E10 bottle are long gone.”

Perhaps this in turn will bring a bit of magic back to the non-vintage segment. After all, you can buy sparkling wine from just about any wine-producing country. Mailloux says the Comte Champagne is embarking on a scheme to bring value back to the heart of Champagne. “We are conducting a strategic reflection called Champagne 2030, in order to move from a volume-based model – which has offered Champagne half a century of growth – to a value-based model.

“Champagne strives to remain the sparkling wine of the highest quality within the sparkling wine market and will continue to exploit and develop the myth around the wines, together with the prestigious historical assets of the region and its awareness and prestige everywhere, including those markets which are still to be developed.”

Mailloux says an appropriate value strategy needs to be consistent across the wine range, including non-vintage Champagne. “It is true that vintage and prestige cuvées still benefit from a beautiful market potential (they only represent 1.8% and 4.2% of the 2012 Champagne shipments respectively), but production of vintage Champagne depends on the yearly yield, because every producer will have to determine which volume goes into the non-vintage blend and which volume goes into the vintage Champagne. Taking into account that only wines from one single year are allowed to be part of vintage Champagne wines, their volume potential is naturally limited.”

Mailloux adds: “When it comes to prestige cuvées, part of their prestige is due to their limited availability and to the high level of attention given by their producers, who do not compromise on absolutely exceptional quality – as a consequence, their availability is limited as well. Lastly, let us not forget the continuous success of rosé Champagne, which represents 9.4% of shipments but 11.4% of value, and continues to experience steady growth.”

Some believe reaching the production ceiling – the ultimate limitation – and the quest for global success will mean consolidation on the ground in Champagne. Jacquart’s l’Anson says the future means “probably some consolidation of smaller producers and growers – there are currently 12,000 registered brands in Champagne, so it is hard for the smaller producer to have a global voice”.

But for those with established brands this is not a concern and Pernod Ricard’s Hotton is gearing up to launch the latest vintages of both GH Mumm and Pernod Ricard. “We will keep on consolidating our position in the main markets, but also developing our opportunities in emerging markets,” he says.

“We currently have two strong international activations for both our brands, such as the Formula One Partnership (for GH Mumm) and Design Miami partnership (for Perrier-Jouët) that enable us to express our brands’ personality consistently and on a global scale.”

Mailloux says all Champagne wines need to continue to benefit from an ever-increasing attention to production and marketing, “because they all represent their appellation which, in return, is being fed by continuous qualitative innovation”.

As is obvious from the UK example, thirst for limited editions, vintages and special cuvées is not the same the world over. In fact, if you were to put the numbers on a chart, it would look more like the scribblings of a seismometer in a major earthquake than a coherent look at the global performance of Champagne’s various sub-categories.

Although it’s clear that quality, not quantity, and therefore value, not volume, is the name of the game, the world is not one when it comes to many things. While Champagne is no exception, we are finally starting to see the magic behind The Prestige.

Related articles: